Although they should only be used as a last resort, 401(k) loans can be a helpful tool to get you through a rough time or to help you contribute to a downpayment for a primary residence. A 401k loan entails taking a loan from your retirement and paying it back over time with money that is deducted directly from your paycheck. Not all 401(k)s allow loans, but many do.

This type of loan typically has a repayment period of 5 years and a limit of $50,000 or 50% of the total you have saved, whichever is smaller, unless you are using the funds to buy a home, in which case the loan repayment period can be 25 years.

In some ways it’s less painful to pay back a 401(k) loan than other types of loans because the automatic deduction leaves very little to take care of in terms of logistics. However, the loan payments will reduce your paycheck, so you need to do the math and make sure that you are able to cover your bills and expenses after the payment is deducted.

While we don’t advise 401(k) loans unless it’s an emergency, in some cases it can be a viable option. For instance, if you have a large unexpected expense that your emergency fund can’t handle and your credit score won’t get you a favorable rate on a personal loan, you may be better off with the 401(k) loan.

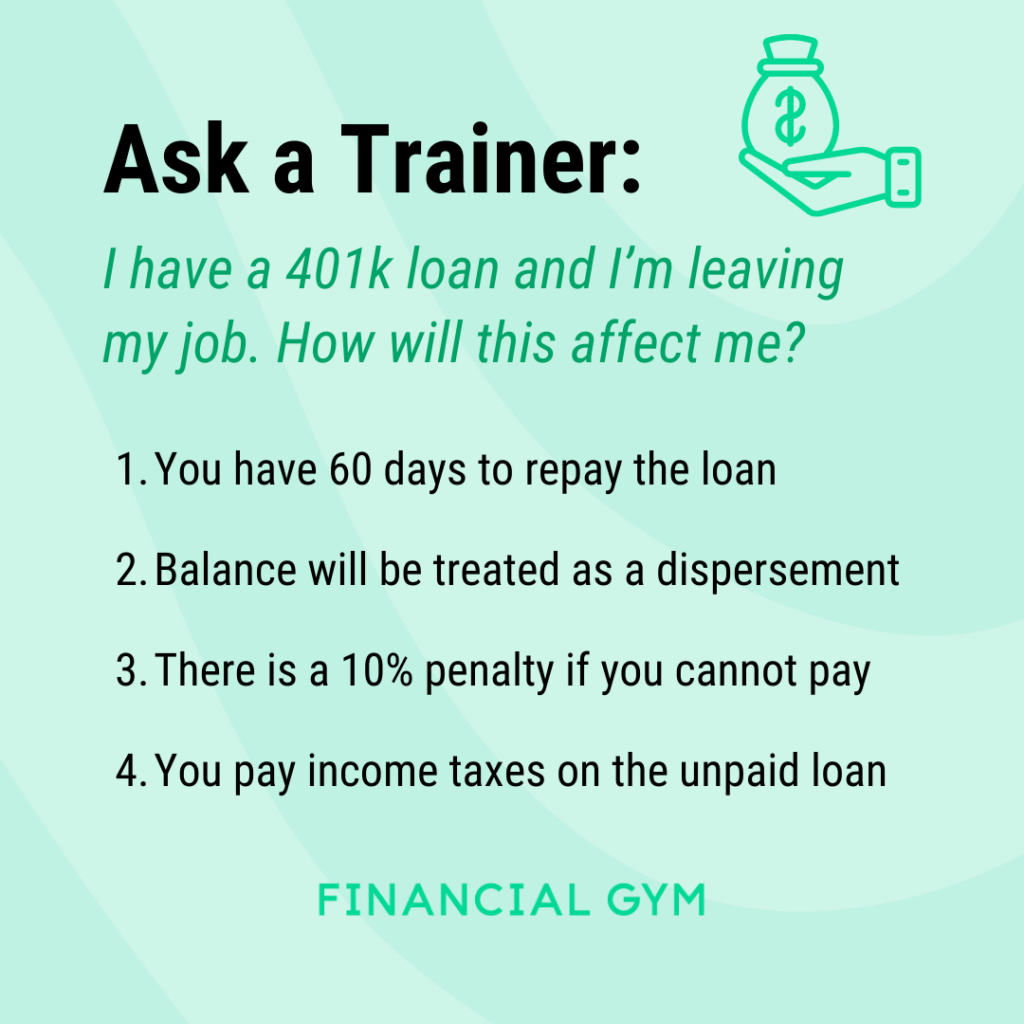

However, this safety net is not without its downsides. If you have a 401k loan and lose or leave your job, you have 60 days to repay it, or you will have to take that as a disbursement, which means you’ll get a 10% penalty and pay income taxes on the funds. This can cost you a lot of money up front and also means that you have the opportunity cost of no longer having those funds working for you as investments. (You can use this calculator to estimate the costs of taking out this type of loan.) You also pay back the loan in after tax dollars, so you have to pay taxes on the funds you use to repay the loan, and you’ll be taxed as income when you draw from them during retirement.

Overall, what this means is that you should avoid 401(k) loans if possible, and if you do take one out, you may want to reconsider a job change until you pay back the loan. Otherwise you can expect to pay a hefty fee if you are not able to cover the balance of the loan upfront.