The Financially Free Blog

4 Things to Know About Financial Challenges in Native Communities

It’s appalling—but unsurprising—that after hundreds of years of stripping Native communities of their land and natural resources, Native Americans still face tough economic challenges. To recognize Indigenous Peoples’ Day, we rounded up news articles, reports, and stats to know about the current state of Native Americans’ financial outlook. A recent poll found that more than two-thirds of Native Americans have experienced “significant financial problems” due to inflation.

How to Improve Your Finances with Just One Tweak per Week

If you have ever struggled or are currently struggling with money, it can feel like you are alone. That could not be further from the truth. Many Americans are living paycheck to paycheck and no one is born financially literate. A 3-6 month emergency fund can look daunting when making ends meet is difficult enough.

Personal finance is personal and it is important to talk to a professional if you need help with your finances. The Financial Gym is a great place to start.

What is Bankruptcy? Debunking 3 Common Myths

Bankruptcy is often held up as the worst thing that can happen to us financially. We are taught to fear it. Creditors have an incentive to make us scared of bankruptcy because it’s the only way to legally wipe away our debts (and their potential profits). Unfortunately, this fear-mongering keeps us trapped in debt and prevents us from building the kind of financial life we want.

Myth # 1: I’ll lose my home or car if I file for bankruptcy

In most cases, people who file for bankruptcy are able to keep their home and vehicle.

4 Tips for a Fall Financial Refresh

There is something about fall that makes it feel like a good time for a refresh. Maybe it’s the changing of the leaves and that crisp fall air—or maybe it’s looking at your credit card statement after all of that summer fun. Either way, it’s worth taking every chance you can get for a reset. Here are four tips to make the most of the time we have left this year.

With only three months left in the year, you can more easily anticipate upcoming large financial expenses. Do you have any travel planned? What will the holiday season look like for you? Are you planning any major home updates?

How to Pay for Medical Intervention Needed to Start a Family

Starting a family can be an exciting—but also stressful. This is especially true for individuals and couples who have to deal with additional costs to conceive a child, including LGBTQIA+ couples, single parents by choice, and hetero couples facing fertility challenges. One of the frustrating aspects of starting a family when you’ll need medical intervention is that you have no way of knowing the final cost when you’re just starting out. The total depends on a number of factors including what medical interventions you need, what your insurance covers, and which clinic you use.

Message from the CEO - My Manifesto

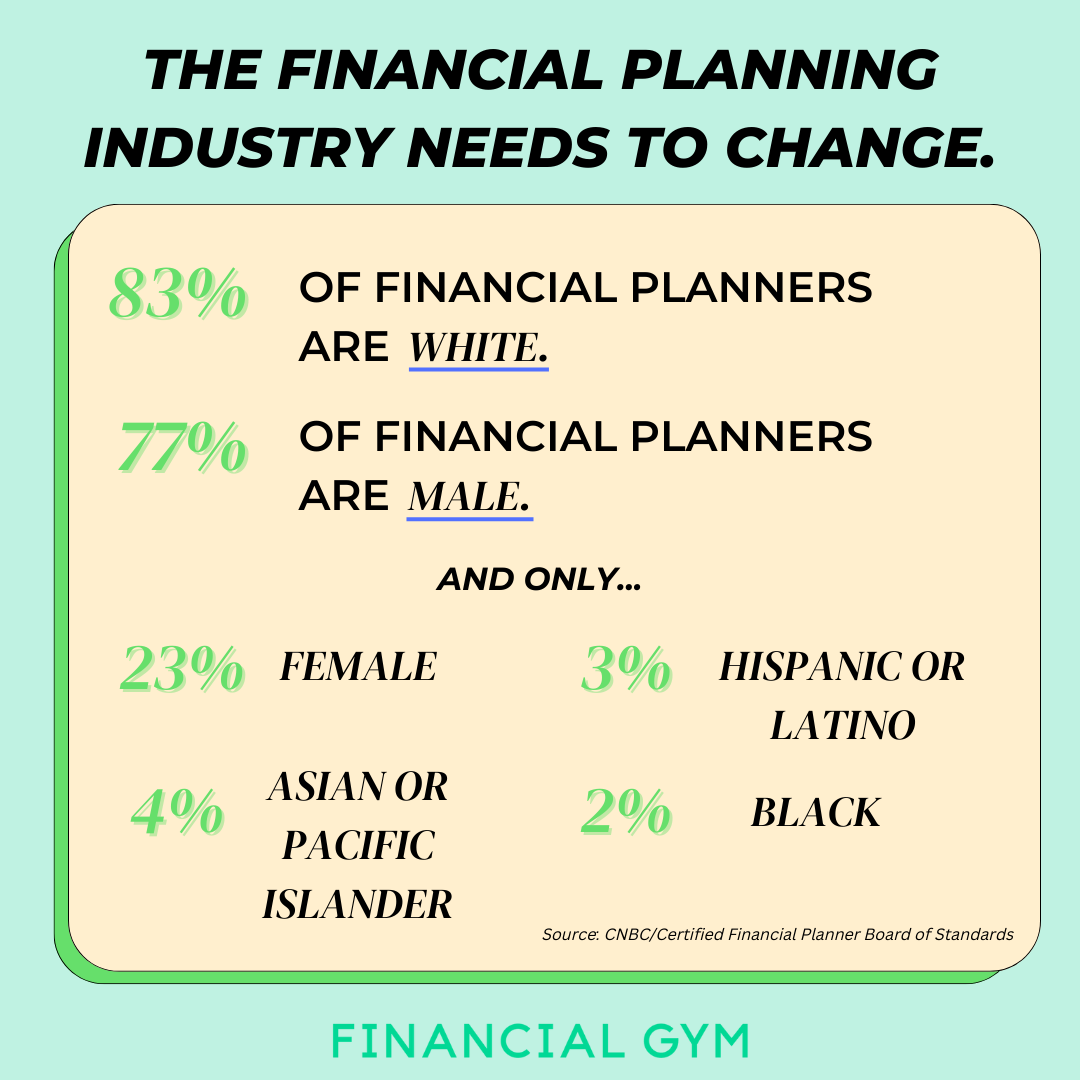

According to data released just last year, 83% of financial planners are white and 77% are male. Financial advisory firms will argue that this is where the wealth is held in the U.S., so they’re hiring to serve this population. I argue that a paradigm shift needs to happen in the wealth management industry. Instead of continuing to help white men and their families grow and preserve wealth, why not coach people and help them to build wealth?

Financial Gym has coached thousands of people from negative net worths to positive net worths in a relatively short period of time.

Could You Benefit from the Limited PSLF Waiver?

With all of the excitement around federal student loan cancellation, we don’t want other federal student loan benefits to be overlooked. In particular, the deadline for the limited Public Service Loan Forgiveness (PSLF) waiver is quickly approaching. Borrowers who believe they may qualify under the waiver have until October 31, 2022 to consolidate their loans (if necessary) and submit their employment for certification. The limited PSLF waiver offers a temporary path to counting certain payments towards PSLF that previously did not count.

5 Ways to Negotiate for the Pay You Deserve

A century ago, women still didn’t have the right to vote. But 102 years ago that all changed with the 19th amendment. The 19th amendment, which gave women the right to vote was signed into law on August 26, 1920, allowing women to use their voice and vote. As of 1973, in honor of this, Congress marked August 26th as Women’s Equality Day.

Though on this day, women achieved equality through having the right to vote, we know that there is still inequality that women face, especially when it comes to earning.

Why Now is the Perfect Time to Start Travel Hacking

A lot of us love to travel. I know this because I’ve worked with hundreds of clients on hundreds of financial plans, and once we work through the hard numbers like assets and liabilities and expenses, we talk through the fun stuff, like goals and non-negotiables. Like me, a lot of my clients’ primary goal is to travel, and it’s a non-negotiable part of living the life we want.

Also like me, they like to travel more than they can afford to. Luckily, there’s a tool for that, and it’s called Travel Hacking. Travel Hacking is the art of using airline and hotel loyalty programs to their full potential, often by using points and miles credit cards strategically.

The Most Underutilized Financial Tool You Already Offer Your Team

Many companies and organizations struggle with how to assist employees in building short-term financial stability. While newer options like employer-sponsored emergency funds can certainly help, most companies already offer their employees an extremely effective savings tool: the ability to split their direct deposits. This tool is underutilized: only 19 percent of employees who use direct deposit split that into multiple accounts. But when employees do split their direct deposit, the overwhelming majority do so to stash cash in savings; nearly three-quarters of employees who split their direct deposit did so to save money.

Ask a Trainer: Should I Invest in a 529 or a UTMA for My Child?

At The Financial Gym, we are often asked by current and future parents how to best save for their child’s future and education. A common vehicle for this is the 529 account, but you may have also heard of an UTMA. Let’s dive into both.

First things first: there are 51 separate 529 plans—one for each state plus the District of Columbia. 529s are also known as Qualified Tuition Programs (QTP). Each 529 has slightly different features or rules as it relates to their respective states, but their purpose is the same.

4 Tips to Cut Down on Your Food Budget this Fall

Besides housing, eating out is one of the biggest line items we see in a client's budget. From fast food to fine dining, eating out can quickly add up and prevent you from meeting your savings goals on time. While we can’t stop eating, planning ahead and having meals at home is the quickest way to cut back on your eating out/ordering in spend.

We’ve collected four tips to help ease the pain of meal planning without sacrificing flavor.

3 Questions to Ask Yourself if You Have a Roth 401(k)

There are a few critical choices we make about our retirement accounts including how much to contribute and what to invest in. Due to the rise in popularity of Roth 401ks, you might have one other important decision: should you contribute pre-tax money to your traditional 401k, post-tax money to your Roth 401(k), or have a mix of both?

Spoiler alert: everyone’s situation is different and there may not be a clear best choice. To decide, you’ll need to make some educated guesses about your answers to the following questions.

Not Impressed with Student Loan Cancellation? This Payment Plan Might Help.

While $10,000-$20,000 in federal student loan cancellation is welcome news for many borrowers, those with larger balances—particularly approaching or exceeding six figures—may feel underwhelmed by the assistance. Fortunately, the Biden administration’s announcement on student loans included provisions that have the potential to significantly ease the burden on borrowers with large amounts of federal student loan debt.

We frequently see clients who want to repay their student loans, but their high balances and unsustainable payments make it feel impossible.

13 Financial Trainer Tips to Get You Back on Track After the Summer

During the summer, it’s easy to be liberal with your spending. After all, there are weekend getaways and impromptu rooftop happy hours, and you want to soak up as much summer fun as possible. By the end of the summer though, once you look at all you've spent that breezy summer attitude may start to fade.

But we are here to tell you it is okay! Although some mistakes in life can't be undone, financial ones usually can. All you have to do is put your summer spending behind you and turn those automatic deposits back on!

What You Need to Know About Credit Line Decreases

Have you ever received a notice from your credit card company informing you that your credit limit has been cut? It happens more often than you’d think. For some people, this is a minor inconvenience. For others, it makes a tough financial situation even more difficult. Either way, it’s important to know that this can happen to you and also be aware of strategies to avoid it and ways to address it if it does happen.

If you’ve never experienced an unexpected credit limit decrease, you may be thinking, “Is that even legal?” Yes, it is.

Here Are 5 Ways to Prevent Lifestyle Creep

If your job gave you a raise next week, what would you do with the extra cash? Would you order the most expensive wine bottle in your celebratory dinner? Go on a shopping spree and buy things you never thought you could afford? For many people, the natural excitement that comes with additional income results in an innate desire to spend more.

This phenomenon is called “lifestyle creep”.

It happens when what you once considered as “enough”, like thrifting your entire wardrobe, is no longer satisfactory after your discretionary income increases. It makes former luxuries — like designer jeans — seem like new necessities. This is often what keeps people in what seems like a never-ending financial trap.

4 Most Important Types of Insurance

Most of us don’t doubt our need for health insurance, and since we don’t have access to universal healthcare, we do what we can to get insured. In lieu of a shift in sentiment that recognizes healthcare as a human right, we rely on health insurance to protect us from having to absorb the full cost of medical care that most people cannot afford on an individual basis.

Health insurance isn’t the only area where we need to focus on managing risks, and decisions about the other types of insurance that we need can feel much more daunting. Just like we want to protect ourselves from illness or injuries, we also want to protect ourselves against the loss of or damage to our homes, or the possibility of interruptions in our salaries if we cannot work for health reasons.

What You Need to Know About Student Loan Cancellation

This week, President Joe Biden announced that his administration will cancel $10,000 of federal students for low-to-middle-income borrowers and up to $20,000 for Pell grant recipients. Naturally, borrowers (including Financial Trainers and TFG clients) are anxious to find out whether they will qualify for the cancellation and what they need to do to get it.

Federal student loan borrowers who earn less than $125,000 or $250,000 for couples will qualify for up to $10,000 in student loan cancellation. Pell grant recipients (lower-income students) are eligible for up to $20,000 in federal student loan cancellation as long as their income is below the threshold. Pell grant recipients who exceed the income limits will still be eligible for $10,000 of cancellation.

3 Questions to Ask When You're Blending Finances in a Relationship

Let’s face it. It’s hard enough to manage finances as an individual. Balancing needs and wants, covering bills and non monthly expenses, and prioritizing which goals to save for first can take up some serious time and mental space. When you add another person into the mix, it can become even harder because there are two people’s perspectives to take into consideration.

As soon as we move past the most basic elements of our existence, figuring out how much to spend on what becomes much more complicated. We all need food and water, but even in those most elemental of categories we can disagree on what our needs are.