Imagine that you are on track with your budget for the month and feeling amazing about it — as you should be! But then you go for your $200 quarterly hair appointment or your $500 annual credit card fee hits, and suddenly, your budget is busted.

These types of expenses feel like surprises, but they aren’t — they are regular, predictable expenses that should be part of your budget. The problem is that we are so focused on monthly budgets that we don’t plan for expenses that occur annually, quarterly, or every few months.

So, how do we include these expenses as part of our budget? The answer is a sinking fund!

What is a sinking fund?

A sinking fund is a way to set aside money every month for a specific future expense. This means that instead of bearing the cost of say, your $600 bi-annual car insurance payment in just two months of the year, you set aside $100 each month so that you have the full $600 each time your payment is due.

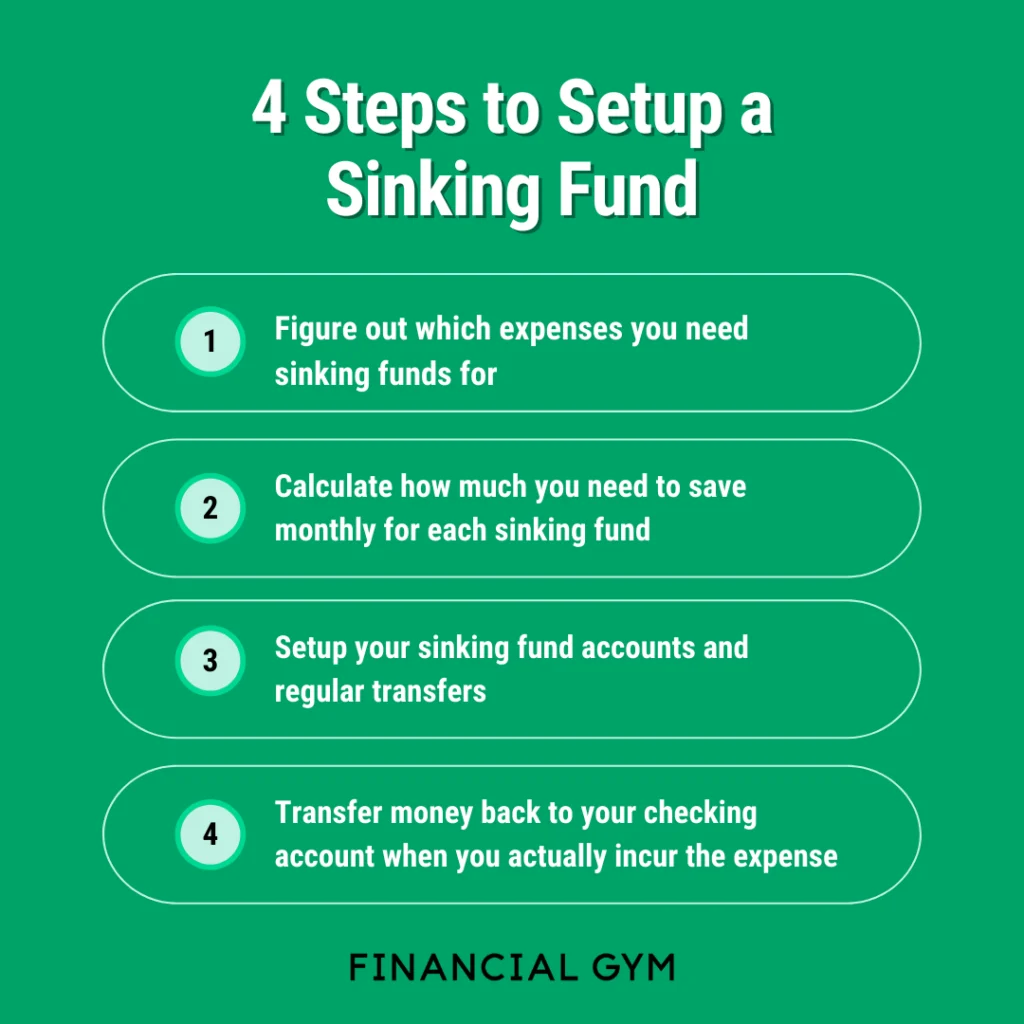

How do I set up a sinking fund?

Step 1: Figure out which expenses you need sinking funds for

Start by thinking about which expenses catch you off guard and leave you scrambling. Maybe it’s holiday gifts or back-to-school shopping for the kids. Here are a few common examples:

-

Non-monthly insurance. Don’t forget about that annual renter’s insurance charge or your bi-annual car insurance.

-

Annual subscriptions. Yes, I’m looking at you, Amazon.

-

Annual credit card membership fees. Even if the perks offset the cost, the annual fee is still coming out of your pocket.

-

Gifts. Holidays, birthdays, Mother’s Day, Father’s Day, weddings — all of it.

-

Hair and other wellness expenses

-

Travel

-

Back-to-school supplies

-

Home maintenance

-

Car maintenance

Step 2: Calculate how much you need to save monthly for each sinking fund

First, you need to know the total annual cost of the expenses you want to create sinking funds for. Some of these, such as annual subscriptions and insurance, are easy to track down while others — such as gifts or car maintenance — take more work. For example, to calculate how much you need for a gift sinking fund, you could look back on how much you spent on gifts last year. Alternatively, you could estimate how many people you buy gifts for throughout the year and how much you spend on each person.

Once you have the total annual cost, divide it by 12 (or the number of months you have to save for the expense).

Step 3: Set up your sinking fund accounts and regular transfers

It’s best to create a separate account for each sinking fund so it is super clear how much money you have for each expense and you don’t end up using money that was intended for car maintenance to pay for back-to-school supplies. While you can do this at any bank that allows you to set up multiple accounts, there are a few that make this particularly easy. With Ally Bank, you can set up separate “buckets” for each sinking fund. One Finance allows you to set up “pockets” that can serve as sinking funds.

To make your sinking funds seamless, set up recurring transfers in accordance with your pay schedule or on a monthly basis.

Step 4: Transfer money back to your checking account when you incur the expense

Keep in mind that if you are transferring between different banks, it may take 3-5 days for the transfer to go through, so plan accordingly!