We’ve all seen the news: the last 2 years of Covid-related upheaval has created quite the housing boom. As many people are able to work from home, many have also decided to relocate, moving out of small apartments or cramped cities to have more space and a place to call their own.

As we tell our clients, buying a home takes a lot of financial preparation. You’ll need to figure out how much you can afford to pay for your mortgage each month and create savings accounts for your downpayment and a contingency fund. In an ideal situation, you’ll put as much down on the house as possible so you can lower your monthly payments and build equity as quickly as possible. In order to avoid paying Private Mortgage Insurance, or PMI, you’d need to put 20% down.

Saving 20% of the cost of a home can be daunting, especially if you live in a high cost of living area. To bridge this gap, there are a few tools you can use to reduce your upfront costs, and one of the most common is an FHA loan.

FHA stands for Federal Housing Administration, and with an FHA loan, your mortgage is backed by the FHA and made through an FHA-approved lender. These loans are available to first time home buyers and can be particularly beneficial to those with less than perfect credit. They also only require a 3.5% down payment, which helps to make homeownership accessible to many people with a low-to-moderate income.

Because of these reasons, FHA loans can seem like a no-brainer, but there are some important things to consider before taking the plunge. Below are some pros and cons of FHA loans to help you determine whether going this route is right for you.

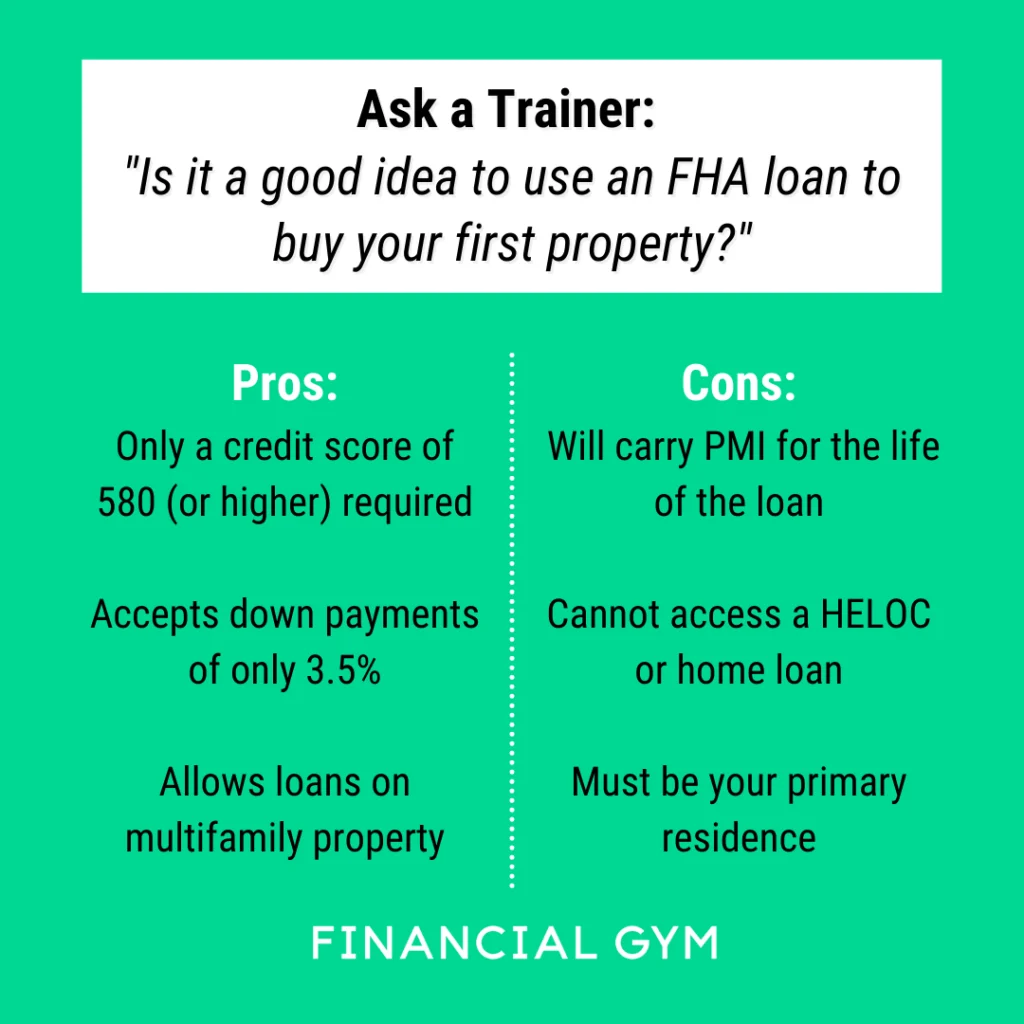

Pros

FHA loans are intended to expand access to homeownership and therefore require lower credit scores. The loans only require a credit score of 580, and even those with a score between 500 and 579 can qualify for a loan if they can make a larger down payment.

Purchasing a first home through an FHA mortgage with a credit score above 580 only requires a 3.5% down payment, which greatly reduces the upfront costs. Those with lower scores can still qualify with a downpayment of 10%.

To make a downpayment, you can use your savings, a grant from a home buying assistance program, or a gift from a family member.

You can get an FHA loan on a multifamily property, which may be able to help you reduce your own housing costs.

Cons

You will carry PMI for the life of the loan, even after you build more than 20% equity. This means in order to stop paying PMI, you have to refinance, which means you will start the amortization clock over and grow your equity more slowly.

Lower down payments mean higher monthly mortgage payments.

You may not have enough equity to access a HELOC or home loan, and therefore will need to have a hefty contingency fund for high dollar costs like repairs.

The property must be your primary residence and owner occupied, so you cannot use an FHA loan on an investment property.

As with all financial decisions, it is important to make sure you are going in informed and understanding your options. Particularly when buying a house, it is also helpful to have the support of knowledgeable people who have no skin in the game. Your real estate agent gets a cut of the sale and may be biased towards getting a more expensive home. Mortgage brokers often approve borrowers for loans so large they are out of touch with a borrower’s financial responsibilities. We recommend finding independent support, or better still, a financial trainer who can help you through the process.