One of the most common concerns of clients at the Financial Gym Advisors is maintaining a healthy credit score. Healthy credit scores can get you a lower interest rate on a mortgage, assure a landlord that you’ll be a good tenant, and help you secure favorable rates on debt consolidation loans or student loan refinancing.

Last week, amidst a financial crisis that has pushed the national unemployment rate to almost 12% and state rates up to 25%, FICO unveiled a new credit scoring index intended to help lenders reduce risk in a time of uncertainty: the FICO Resilience Index, or FICO-RI.

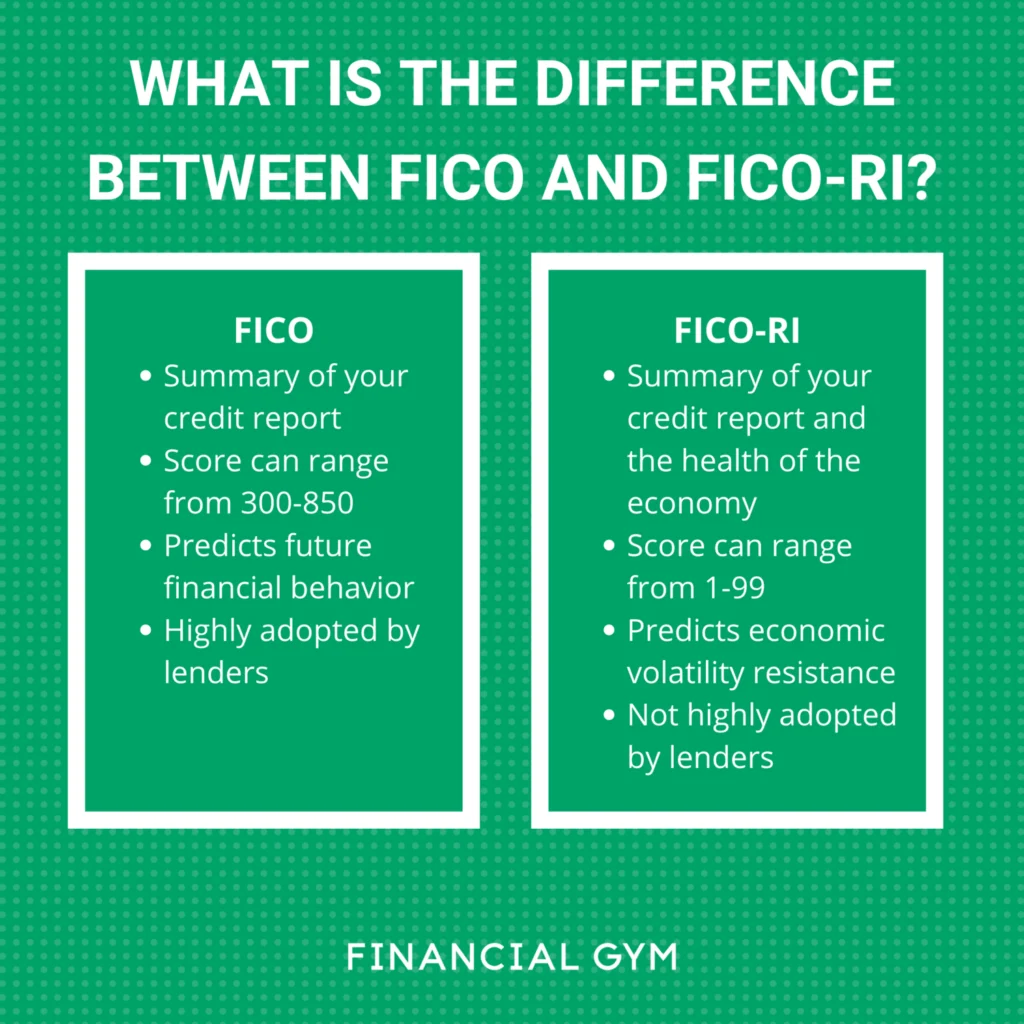

The FICO-RI differs from the FICO score in a few ways. Your FICO score is essentially a summary of your credit report. It’s based on a scoring model that projects the likelihood that you will be more than 90 days late on your debt payments in the next 2 years. Borrowers with the least likelihood of delinquency get the highest scores, and therefore more favorable lending agreements. In short, your past financial behavior is used as a predictor of your future financial behavior.

The FICO-RI looks at all of the factors that go into your FICO score, but it also takes into consideration the health of the economy. Instead of just looking at your past financial behavior, it looks at the ways that borrowers with your credit profile performed throughout and since the Great Recession. Based on this analysis, borrowers are given a score from 1-99, where 1 is the best or “most resilient” and anything over 70 suggests a borrower is “very sensitive” to economic volatility.

While this is a new development and we can’t know exactly how it will play out for borrowers, we can assume a few things will be true. Above all, your utilization rate will play a huge role in your score. It’s hard to manage economic volatility when your credit cards are maxed out and your payments are high. We can also assume that the length of your history will be important. If you have a short history it is difficult to gauge how well you would behave in a crisis because you may not have dealt with one yet. Unsurprisingly, a history of late payments will suggest you’re less resilient.

What this will mean for everyday borrowers is uncertain. First, we don’t know whether financial institutions will uniformly adopt the FICO-RI in their lending practices, or how soon, or how much of a role they will play. Second, this isn’t replacing FICO scores or any other type of credit scoring, it is just adding a layer of complexity to the credit profile as a whole. That aside, we can reliably make some predictions.

Most people with Very Good or Excellent credit (above 680) will continue to have good scores with FICO-RI and will continue to get access to financial products much like they did before. It is also likely that those with Poor credit scores will experience more of the same difficulty accessing loans and other types of credit. Greater questions arise on the “in between” area of Fair to Good credit between around 580-680. This group is much more likely to fall into the “Sensitive” range and could experience a negative impact due to FICO-RI.

So what can YOU do to protect or work towards a healthy credit profile? This is the one straightforward answer in the mix: the same things you have been doing.

-

Make your payments on time. If you can’t, contact your lender to see if you can work out a payment plan you can work with so you can prevent negative remarks on your credit report.

-

Improve your utilization rate, and avoid using too much of your credit on each individual card as well as spread out across your credit limit as a whole.

-

Make sure your oldest cards are in good standing and that you are using them. Users are reporting an increase in accounts being closed for non use, a move card issuers are making to reduce their own risk profiles.

-

Remember that keeping accounts active doesn’t require you to carry a balance, it just means you have to use the card and pay it off, which you can do in one statement cycle without ever accruing interest.

What FICO-FI means for the average person remains to be seen, since it is too new to study. However, we CAN rest assured that the advice you’ve been getting from your trainers still holds true. If you want to make sure you are in good shape or see what you need to do to improve your standing, talk to your trainer. They can help you look through your credit history and see if there are ways to improve your overall profile. They can also help you to make a plan to improve your scores over time and make sure you are doing the most with what you have to work with, wherever you are on your financial journey. We’re here for you!