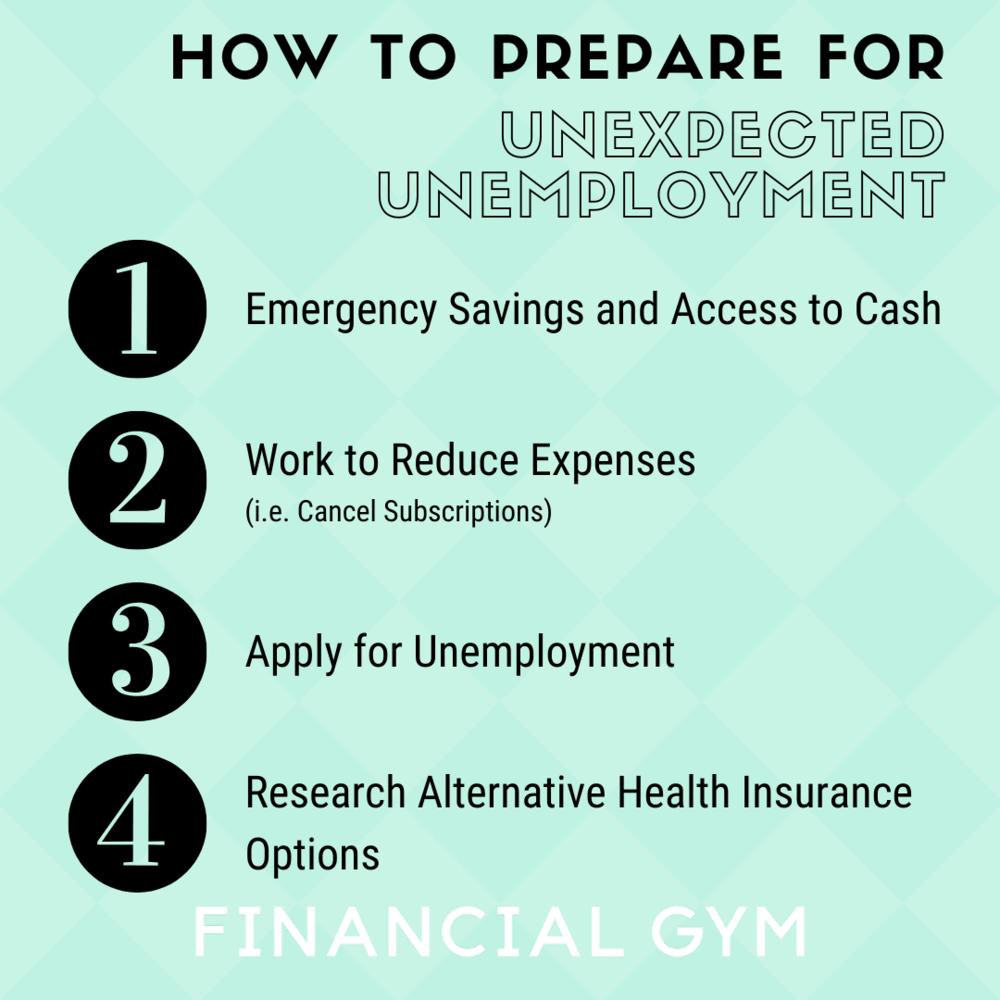

During these unprecedented times, many people have found themselves unexpectedly unemployed. Here are our tips for navigating unemployment:

Emergency Savings and Access to Cash

Ideally, we recommend you have a full 6 months of fixed and variables expenses saved in cash, preferably in a high yield savings account. This ensures that if you lose your job, you will be able to support yourself without having to drastically change your lifestyle. Sometimes, however, this isn’t possible, so how else can you access cash quickly in times of need?

-

Check to see if you have uninvested cash sitting in your personal brokerage accounts (if you have one).

-

Check to see if you have any matured savings bonds that can be cashed in. These are not too popular now, but they were popular gifts 20-30 years ago. You may have received them for birthdays, holidays, or special occasions so check with your parents to see if there are any of them lying around that can be cashed in!

-

Pull money from restricted accounts, like Certificates of Deposit (CDs). Typically, a CD has a set maturity date, but you are able to withdraw money early if you absolutely need to. You will have to pay a penalty, but it usually just means you need to forgo some of the interest earned, so you will still be able to access your original deposit.

-

Open a credit card with 0% interest for 12 months. This is a last resort, but sometimes a necessity! This will allow you to make purchases and not incur interest charges for a year. The card should still be used sparingly, but it’s a much better option than using a credit card that has a high interest rate.

Expense Management

When unemployment hits, you need to make every effort to reduce your expenses in order to make whatever cash you have last as long as possible.

-

Work to reduce fixed expenses.

-

Cancel or freeze subscriptions and memberships.

-

Call service providers (cell phone/internet) and negotiate lower monthly rates.

-

Reduce debt payments as much as possible.

-

Put student loans into deferment or forbearance if possible.

-

Transfer credit card balance to cards with 0% interest for at least 15 months if possible.

-

Request hardship assistance from debt companies (reduced interest rate and/or lower minimums).

-

Request mortgage forbearance or hardship assistance.

-

-

-

Cut variable expenses as much as possible.

-

Challenge yourself to multiple no spend days each week.

-

Get creative and cook the food you have at home!

-

-

Adopt a cash budget and set a weekly allowance for variable expenses.

-

Try to stretch every dollar as far as you can! Set budgets for necessities like groceries and household supplies and portion out the remainder for more “fun” expenses like going out with friends and shopping.

-

-

Adopt a DIY mindset!

-

Start doing your own personal care (i.e. manicures, haircuts, eyebrows, etc), or ask a friend who has more experience!

-

-

-

Get Creative!

-

If possible, rent out your apartment on Airbnb or other similar sites and move in with friends or family members.

-

Rent out your car or parking space, if you have one!

-

Sell clothes, electronics, and furniture online using sites like Poshmark, The Real Real, Facebook Marketplace, etc.

-

Income Management

Just because you no longer have full-time income, doesn’t mean you can’t stop managing the money that you do have! You should be thinking of ways to “make” money until you are able to find another full-time job.

-

Negotiate your severance package. Assuming, you are not being let go for poor performance or for violating company policies, you should be able to negotiate with your employer to get them to provide you with severance pay and some other temporary benefits. At a minimum, you should get 2 weeks pay, but most companies have standard severance policies, so check with your HR person and read through the formal documentation.

-

In addition, you should request your employer pay for 1-2 months of healthcare coverage so that you don’t have to worry about that expense right away.

-

-

Apply for unemployment benefits right away!

-

Right now, the waiting period on unemployment benefits is being waived, but typically, it takes a while for these to get processed. You should also note, that if you are receiving your severance intermittently (i.e. paid out weekly), you can’t apply for unemployment until after that ends.

-

Opt to have taxes taken out upfront so that you don’t have to pay them later on.

-

Only take the payout when you need it! If you skip a week here or there, you can extend the amount of time the benefit will last.

-

Actively search for work! You are only eligible to receive the benefits if you are looking for work.

-

-

-

Pick up part-time work where you can.

-

You can still receive unemployment if you are working part-time, so try and pick up some kind of part-time work. Even if it is just a day or two here and there every little bit helps!

-

Make sure you are covered!

Health insurance can be expensive! There are several options to consider once your employer’s benefits expire.

-

COBRA (Consolidated Omnibus Budget Reconciliation Act) allows for you to continue using the same benefits provided by your employer at your own cost. It is usually extremely expensive, when compared to other options.

-

State exchanges allow you to purchase health insurance at a much cheaper rate, but the coverage is often significantly less than what most employer plans provide.

-

If you have pre-existing medical conditions and need good coverage, the cheap plans from the state exchanges likely carry high out of pocket costs, so weigh that against the monthly cost of COBRA before making a decision. Remember to negotiate with your employer to see if they will cover the COBRA expenses for a period of time!

-